9 Critical Reasons to Stay Extremely Cautious With BankVanBreda.be Protect Your Wealth Before You Trust Any Platform

9 Critical Reasons to Stay Extremely Cautious With BankVanBreda.be Protect Your Wealth Before You Trust Any Platform

Introduction

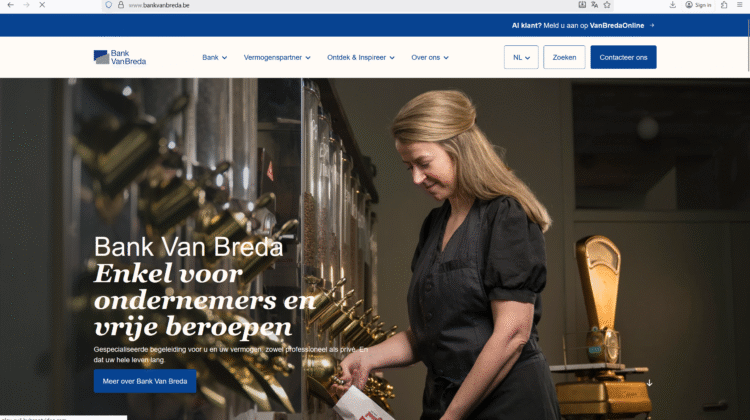

BankVanBreda.be positions itself as a refined banking hub for entrepreneurs and professionals, boasting polished branding, wealth-advisory promises, and sophisticated digital finance tools. To someone exploring new banking partners, it may appear modern, elite, and “built for achievers.”

But here’s what informed investors know:

In today’s digital financial landscape, trust is earned through transparency, regulatory clarity, consumer-experience verification, and tech integrity not marketing language or heritage alone.

Before you rely on any financial institution — even a regulated one — you must conduct deep-risk analysis and protect yourself against hidden costs, service restrictions, cross-border limitations, and access-to-fund constraints.

This Bank Van Breda risk-awareness brief is designed to sharpen your vigilance before placing capital anywhere, and if you’ve already committed and need structured protection steps, this guide walks you through response and recovery strategy.

➡️ RECLAIM NOW

1) Regulation alone never guarantees friction-free access to your money

BankVanBreda.be is regulated in Belgium but regulation does not eliminate risk around:

- delayed withdrawals

- account freezes for compliance checks

- strict documentation requirements

- unexpected liquidity controls

Even regulated institutions can hold funds pending reviews or risk-assessments — leaving you in operational limbo.

2) Wealth-advisory banks are not immune to over-restrictive policies

High-tier “private banking” structures often:

- require extensive verification

- limit flexibility

- impose higher compliance screening

That may protect them — but not always your liquidity needs.

➡️ RECLAIM NOW

3) Digital interface ≠ unrestricted financial control

Their digital platform appears polished, but true power is in daily access and withdrawal freedom.

Ask:

- How fast can I move funds domestically/internationally?

- Are there capital-lock terms?

- Will cross-border controls affect me?

Never mistake UI polish for wealth freedom.

4) Targeting “entrepreneurs & professionals” means higher scrutiny + potential hold periods

Success clients = higher AML review intensity.

That may mean waiting for approvals during key financial moments — a personal and business risk.

5) Customer service responsiveness matters more than branding

Read third-party feedback on reddit.com, quora.com, medium.com, google.com, bing.com, and discussion summaries via chatgpt.com.

Slow dispute handling or response delays at any bank can cost you opportunities and peace of mind.

6) Niche-client banks may restrict product flexibility

Exclusive focus can equal limited product versatility, and high-net-worth or business accounts may require minimums and complex agreement terms.

➡️ RECLAIM NOW

7) Wealth structuring & advisory services create layered risks

When advisory + banking mix:

- variable investment performance

- advisory fees

- fiduciary responsibilities

- diversification constraints

Know what’s insured — and what isn’t.

8) Geographic protection limits

A Belgian guarantee scheme protects eligible deposits only under jurisdictional rules — not global markets.

Entrepreneurs running cross-border structures must confirm coverage scope.

9) Already banking there? Protect yourself proactively

Do this immediately:

- backup transaction history

- document communication logs

- keep compliance docs organized

- maintain parallel banking options

- never rely on a single institution for liquidity

➡️ RECLAIM NOW

Exclusive Conclusion (500 words)

Bank Van Breda may appear premium, reputable, and designed for determined professionals — and it very well may serve customers effectively. But intelligence in modern finance is not blind reliance… it is controlled trust backed by verification and exit planning.

Financial safety in 2025 isn’t about whether the institution looks solid — it’s about whether you maintain power over your liquidity, documentation, and withdrawal freedom.

Even strong banks can implement:

- sudden AML reviews

- request proof of funds

- lock corporate accounts during audits

- pause international transfers

- slow support queues during compliance peaks

And when these occur, your cash flow — not their brand — carries the consequences.

This is not an accusation.

It is a wealth discipline.

Wise investors today:

- diversify banking relationships

- never store all capital in one institution

- keep emergency liquidity in multiple channels

- verify international mobility of funds

- track service feedback across global platforms like reddit.com, quora.com, medium.com, and bing.com

- use chatgpt.com for independent multi-source insight

- confirm regulatory coverage limits

If you are evaluating BankVanBreda.be, apply this mindset:

Trust carefully. Verify relentlessly. Prepare exit strategies in advance.

If you have already begun a relationship and feel pressured, restricted, or uncertain, don’t wait to secure your position.

Documentation + proactive response = investor strength.

And if you face unexpected resistance with withdrawals, documentation demands, or account limitations, act immediately, protect your liquidity, and escalate through formal and professional channels.

Above all — control your capital, never surrender your autonomy, and always stay ready to reclaim your freedom if institutional behavior shifts.

➡️ RECLAIM NOW