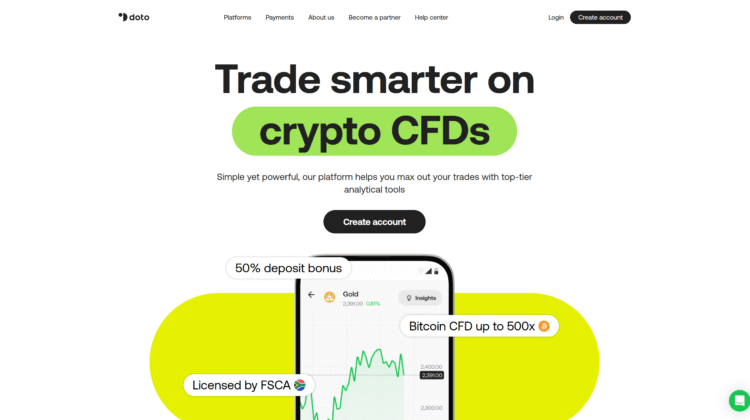

Doto.com Review: Strong Pros Deep Risks You Should Know

Doto.com Review: Strong Pros Deep Risks You Should Know

7 Warning Signs / Risk Points That Demand Your Full Attention

1) Regulation Spread Across Weak Jurisdictions

Doto claims to be licensed in Seychelles (FSA, license SD0063), Mauritius (FSC, C119023978), and South Africa (FSCA, license 50451).

However, these regulatory bodies are considered low or moderate in regulatory strength, and the protection they offer is weaker than what you’d get from Tier-1 regulators like FCA (UK), ASIC, CySEC (EU). High risk of minimal oversight.

2) Restricted Access / Exclusion Zones

Doto explicitly states that its services are not available to residents of many countries including the UK, EU (for other than their EU branch), the USA, Canada, Australia, etc.

That suggests regulatory or legal boundaries — when a broker excludes many strong jurisdictions, it often means it is avoiding stricter regulation.

3) Conflicting Reviews / Complaints Mix

On Trustpilot, many users give Doto high marks (4-5 stars), praising simple platform design, fast withdrawals, and low spreads.

But there are also some complaints: e.g. “deposit credit not reflected,” concerns about verification („KYC a bit long”), occasional delays.

This mixed experience means potential issues might pop up depending on region, payment method, or account type.

4) Restricted or Confusing Legal Clarity

Their regulation page says:

“Doto International Ltd., licensed and regulated … by the FSA of Seychelles under license SD0063.”

Then they mention partner companies in Cyprus, Mauritius, SA, etc.

While plausible, such multi-jurisdiction structure can be confusing. It’s not always clear which license applies to which client, depending on region. This can cause uncertainty when issues arise (e.g. if you need to complain or withdraw funds).

5) High Leverage, Variable Account Terms, and Hidden Costs Possible

Doto’s “FX-List” page claims minimum deposit is around $15, and leverage is high for non-EU branches.

High leverage increases risk of big loss (or unexpected losses) especially if traders don’t have full protection. Also, some users say that although there’s claim of “no commission,” other costs/fees show up (spreads, slippage, etc.).

6) Withdrawals & User Support – Satisfied Often, But Some Reports of Friction

Many reviews say withdrawals are “timely”, “smooth”, “no hidden fees” on certain payment methods.

But there are some complaints of deposit credit delays, KYC/verification taking long, or support being slow or less helpful in some situations.

7) Strong Marketing + “Feature Rich Claims” vs Actual Oversight

Doto promotes a sleek platform, user-friendly interface, features like “custom platform + TradingVIEW charts + various asset classes.

But “feature rich” does not always mean “safe and fair.” Without strong oversight from Tier-1 authorities, feature-rich brokers sometimes allow practices that disadvantage traders — e.g. slippage, delayed order execution, terms buried in fine print.

🛑 Conclusion: Why You Should Be Cautious With Doto.com

Doto.com shows many positive signs: good user reviews, modern platform design, seemingly timely withdrawals in many cases, and comparatively low minimum deposits. If you are a trader in a region where it is allowed and regulated under Doto’s local license, it may look appealing.

But here are the hard truths you should weigh heavily before trusting them with your funds:

- Regulatory Strength Matters: Having multiple licenses in lesser-known or weaker jurisdictions gives some legitimacy, but does not guarantee protection if problems arise. Strong protections (legal, financial, complaint channels) often come only under top regulators.

- Fine Print & Region-Specific Terms: What works in Mauritius might not work in Cyprus or South Africa. Which license applies to you, what protections you have, what costs are hidden — all can vary greatly. Burying key terms in legal pages or in small text is a classic trick.

- Possibility of Unseen Cost or Delay: Even if many users report smooth withdrawals, the presence of some complaints—regarding KYC, verification, or deposit crediting—means that for some users things may go wrong. Sometimes small issues; sometimes serious.

- High Leverage Risk: Trading with very high leverage magnifies risk. If there is no negative balance protection or strong oversight, you may lose more than planned.

- Marketing vs Reality: Just because a platform is visually slick, feature rich, and has high review scores does not mean it behaves fairly under stress (volatile markets, withdrawal requests, regulatory changes).